Wednesday, July 31, 2019

Tuesday, July 30, 2019

Thursday, July 25, 2019

Tuesday, July 23, 2019

Monday, July 22, 2019

Sunday, July 21, 2019

Thursday, July 18, 2019

Wednesday, July 17, 2019

Monday, July 15, 2019

Sunday, July 14, 2019

Saturday, July 13, 2019

Thursday, July 11, 2019

Case Study. Do you know any successful, married property managers? Other than LJ Gilland Real Estate :)

CASE STUDY

MaryAnn was already in real estate when they got married, and Andrew was working for a large corporation as an engineer. He had a nice corner office downtown and even his own parking spot. Then, he got laid off in 2000, during the burst of the dot-com bubble. This was scary for MaryAnn who wondered if her business could support the both of them while he looked for a new job in his field.

They created something good from a bad situation.

MaryAnn needed a website and a lot of technical support. So, she suggested that Andrew work for her company while he looked for his next job.

She was concerned that he was giving up some huge potential career opportunities, but after 20 years as an engineer, Andrew stopped looking for a new job and really became involved in Hoffman Realty.

They realized they were having fun working together. So, they took the plunge and officially went into business together.

Establishing a Routine and Setting Boundaries as Married Property Managers

In his former job, Andrew did a lot of traveling and when he would return home, it was difficult for him and MaryAnn to fall back into the routine of being together. Now that they work together, there’s a lot more harmony around the house. The couple is really in sync and everything runs a lot smoother.

There’s more of a connection within their professional and personal relationship. If MaryAnn is having a bad day, Andrew gets it. There’s a lot more intimacy when you know what each person is going through and what they’re dealing with on a daily basis. They help each other, and they rely on their own individual strengths to keep the company – and the relationship – on track.

Setting boundaries is also important. Married property managers bringing in their spouse to work with them might be concerned that their partner will try to take over and change everything.

That’s not what you want.

Andrew and MaryAnn decided that they would separate which parts of the company they were each responsible for running. MaryAnn is the people person and makes routine decisions about the business. Andrew handles the technology and the high level decisions and everything related to their marketing systems and processes.

In 20 years, these married property managers haven’t stumbled, and it’s largely because of those clear boundaries.

MaryAnn says she admires Andrew’s ability to handle what he handles, and she loves managing her end of the business. She doesn’t flinch when angry owners yell, but she has no interest in figuring out why a computer isn’t working.

Their strengths are much different, and they use those differences to make their company run better.

An organizational chart is more important than ever when you’re married property managers, even if you’re the only two people in the company. Write your name in each box that represents your responsibilities, and make sure you’re not both in the same box.

That’s where conflicts can arise.

If you listened to our recent podcast with Melissa Prandi, you’ll remember what she said about putting together a great property management team. She said make sure you hire people with different strengths. At Hoffman Realty, Andrew and MaryAnn value the separate things that they each do best.

When you decide to work with a spouse or a partner, make sure you can identify which jobs you are each responsible for, and then don’t creep over into each other’s areas. If you have the same strengths and weaknesses at your spouse, maybe you shouldn’t work together. Or, you should be prepared to hire people who can fill in those blanks.

Do These Married Property Managers Ever Get Tired of Each Other?

Working as married property managers doesn’t necessarily mean that you’re together 24 hours a day and seven days a week. While there may be challenges to sharing both a home and a business, you can make it work.

MaryAnn and Andrew think it’s fun to be together. They like laughing about work things at home. They enjoy opening a bottle of wine when necessary to talk about challenges or issues that are happening at the office.

It’s also important to maintain separate identities outside of work. You each need your own passions and hobbies. For example, Andrew loves sports. He’s always at football games or watching hockey. MaryAnn has a great circle of her own friends and is very involved with her children.

You can’t be together all the time. MaryAnn and Andrew have managed not to bring work home unless they want to work on something together. They respect each other’s private time and passions.

When you have other interests, you’re not in danger of getting tired of each other at home or at the office.

Working together makes both of them happy. They have a good relationship in the workplace and romantically. Part of the reason is that they have their own separate identities when they’re not working or together.

Time Management and Work/Life Balance

Working together also allows MaryAnn and Andrew to balance their time better. When she was doing real estate and property management but Andrew was working his corporate job, he would rarely understand why she had to take work calls on the weekends. He didn’t understand then what he understands now. If an owner calls at 7:30 in the morning and is ready to sign a management agreement, MaryAnn is ready to get over to the property, and while Andrew might have once suggested that it wait – he now understands the urgency.

Andrew says that when they had separate careers, it was difficult to understand the work/life balance challenges of the other person. Now, they understand each other completely.

They can also be as flexible as they want with their schedules. Sometimes they’ll take a few days off where they check their emails and handle urgent business early in the day and then spend time bike riding or swimming.

When One Manages the Other

In the beginning, MaryAnn was Andrew’s boss. He didn’t know the industry, and he had to learn a lot.

For example, Andrew has a need to fix things right away. MaryAnn had to coach him in and show him that sometimes people just want to be heard. If they’re upset and complaining, you need to let them keep talking because the problem they’ve called to complain about isn’t always the real problem. You need to give it time and dig a little deeper.

It’s possible to give feedback without being negative and critical. This is something you should set up as a rule. They give each other structured feedback in a way that doesn’t blame or accuse. They adopted the same practice with their employees. It’s effective and it’s kind. It also helps its employees. They can understand things from many different sides and attack a problem without feeling defensive.

MaryAnn, who has a psychology degree, says it’s important to say:

“When you do ______, I feel _______.”

People you disagree with aren’t necessarily doing something wrong. They may just do things differently.

Figuring out the Financials

One of the most important things for married property managers to think about when they go into business together isn’t necessarily the company or the relationship – it’s financial security. When both of you are in one industry and there’s a downturn, you’re both going to be affected.

This happened from 2007 to 2009 when things became difficult in the real estate world. Andrew and MaryAnn had a nest egg, but they were concerned about keeping the company afloat, and they stopped spending money that they didn’t have to spend.

The couple had just completed construction on a house that they planned to move into, but MaryAnn had a gut feeling that they should sell it. So, they did, and they made a great profit. That profit saw them through the hard times of the real estate downturn.

When you work together, you don’t have any diversity of income. That can be a risk, and you might not realize how likely it is to happen.

A lot of this will be completely out of your control. In 2017, it looked like Tampa was going to sustain a direct hit from Hurricane Irma as a category 5 storm. The hurricane turned and the Tampa area got soaked but they were spared the damage they were expecting. It would have been devastating to Hoffman Realty and many of the properties they manage. A lot of property managers in Tampa were wondering if they would be out of business after that hurricane.

The lesson? Plan for what will happen if and when both incomes are lost.

Things to Consider Before you Work Together

Andrew and MaryAnn have some things for couples to think about before they go into a property management business together.

- Do you get along now?

- Do you enjoy working long hours?

- Are you ready to hire more people?

- Do you have insurance?

- Are you financially secured for this risk?

You have to get along already. If you don’t, this isn’t going to fix your relationship.

Andrew suggests putting your foot in the water before you take the plunge. He helped out in the business while he was still looking for other work. So try it out if you can. Have a Plan B if it turns out you’re not meant to do this together.

The insurance is a big deal. When Andrew worked as an engineer, they enjoyed his corporate benefits. When he joined Hoffman Realty, they had to find health insurance and other benefits. Make sure your company is profitable enough to offer strong salaries and good benefits. What will you do for retirement? Think about the long term.

MaryAnn recommends having enough money saved to get through at least two years of an industry downturn. When they suffered through a slow period, they wanted to preserve the business. They cared about paying their employees even when business was lacking. Make sure you’re in a strong position personally and as a company.

Making a Family Business Attractive to Owners

Another benefit to working together is that owners love the idea of working with a family business.

They feel better about leaving their biggest asset in the hands of a locally owned and family-run company. Everyone tells Andrew and MaryAnn that they want local management, not a huge national company.

Most owners know that a family business is going to care about their reputation within the community. When Hoffman Realty selects vendors, they always look for mom and pop businesses instead of huge companies where the customer seems to matter less.

While Andrew is often the face that potential owners see in the blogs and marketing videos created by Hoffman Realty, they are moving to a new, larger space and the plan is to have MaryAnn more visible as well. They also want to have their employees contribute to future blogs and marketing materials.

It’s hard, though, because Andrew’s British accent makes him sound like he knows what he’s talking about.

Of course, he does know what he’s talking about, and so does MaryAnn. If you have any questions about how to work with your spouse or run a successful business while maintaining a successful marriage, these two are the people to speak with. Best Regards

Linda 姬琳达珍 and Carlos Debello

(LREA)

LJ Gilland Real Estate Pty Ltd

PO BOX 19

ZILLMERE 4034

Ph: 07 3263 6085

ZILLMERE 4034

Ph: 07 3263 6085

0413

560 808

0400

833 800

0409 995 578 (L)

Wednesday, July 10, 2019

https://www.smh.com.au/national/suburban-defamation-boom-time-for-lawyers-20190707-p524wt.html

#Unit 5/30 #Tamar Street, #Annerley, QLD 4103 2 2 2 #VENDOR #REVIEW #Overall #Satisfaction #FIVE #STARS #Very #helpful #Recommended by GabrielleBobWilliams 23 May 2017 Carlos and Linda were very helpful with #management and final #sale of our #property. They always #communicated promptly and kept us #informed of any concerns and #responded #quickly to any #repairs or issues. Very helpful - LJ Gilland Real Estate agent review | RateMyAgent http://mvnt.us/m347704

Best Regards

Linda 姬琳达珍 and Carlos Debello (LREA)

LJ Gilland Real Estate Pty Ltd

Linda Debello LREA推荐书LJ Gilland房地产

http://ljgrealestate.com.au/testimonials/

Request FREE Rental Appraisal here!

"Your Local Property Management & Sales Specialists"

PO BOX 19

ZILLMERE 4034

Ph: 07 3263 6085

0409 995 578 (L)

http://ljgrealestate.com.au/competitive-commission/ http://ljgrealestate.com.au/property-management/

http://www.facebook.com/ljgrealestate

Tuesday, July 9, 2019

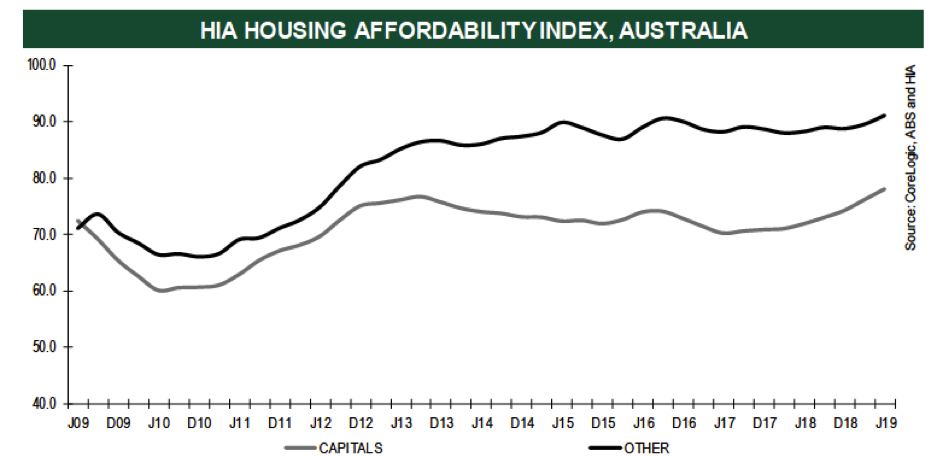

Housing affordability best since 1999, say HIA All eight capital cities saw an improvement in the Housing Industry Association Affordability Index for the June 2019 quarter, with Darwin showing the greatest improvement, its index up by 4.8 per cent.

Housing affordability best since 1999, say HIA

All eight capital cities saw an improvement in the Housing Industry Association Affordability Index for the June 2019 quarter, with Darwin showing the greatest improvement, its index up by 4.8 per cent. Combination of lower home prices, improvements in wage growth and lower interest rates have contributed to the ongoing improvement in the HIA Affordability Index for the June 2019 quarter, according to Housing Industry Association (HIA) Senior Economist, Geordan Murray.

All eight capital cities saw an improvement in the HIA Affordability Index for the June 2019 quarter, with Darwin showing the greatest improvement, its index up by 4.8 per cent. This was followed by Melbourne (+3.0 per cent), Perth (2.6 per cent), Brisbane (+2.6 per cent), Sydney (+2.4 per cent), Canberra (+ 2.4 per cent), Hobart (+ 2.2 per cent) and Adelaide (1.0 per cent).http://ljgrealestate.com.au/property/36-grand-terrace-waterford-qld-4133/?lang=es

HIA’s Affordability Index is calculated for each of the eight capital cities and regional areas on a quarterly basis and takes into account the latest dwelling prices, mortgage interest rates, and wage developments.“For a home buyer with an average income purchasing a median-priced dwelling (assuming a 10 per cent deposit), mortgage repayments will consume the smallest proportion of their earnings since 1999,” added Mr Murray.

“The main reason the HIA Affordability Index today is comparable with the level in 1999, despite house prices rising significantly faster than incomes, is that interest rates are 4.6 per cent today compared with 6.7 per cent in 1999.

“Average earnings have increased by 113 per cent over the 20 years to 2019, while the median home price has increased by 228 per cent but the lower interest rates have kept the cost of servicing a loan the same," he said.

Source: HIA

“There are also a number of initiatives that do not feed into this Affordability Index that will assist with first home buyers entering the market. The reduction in income tax, the easing of APRA restrictions on mortgage lending and the Australian government’s First Home Loan Deposit Scheme are likely to be important considerations for households.

“Despite a significant improvement in affordability Sydney remains the least favourable market in the country, requiring 1.8 times the average income to service a mortgage on a typical Sydney home,” said Mr Murray.

TWO STRATA

TITLED 4 BED HIGH SET STRATA TITLED UNITS WITH PROPERTY RETURNS OVER $52,000 A

YEAR.

AN

OPPORTUNITY HERE FOR AN ASTUTE INVESTOR – YIELDS OVER 5% EACH PROPERTY AND

INCOME

PRODUCING STRATA TITLED AIR-CONDITIONED 3 BEDROOM DUPLEX'S WITH STUDY NOOK

GREAT FOR YOUR SUPERANNUATION

PORTFOLIO! CAPITAL GROWTH ASSURED!

AND THE RENT HAS GOOD POTENTIAL TO MOVE UP 5-10%

Each

house/dwelling is separately titled, as houses on any estate.

You

can do anything internally that meets the local council rules.

Body

corporate only exists to ensure each owner has a say in the external

presentation of the duplex. The Vendor is not aware of any joint costs for

services, other than building insurance of the duplex is paid by the Body

Corporate for both dwellings.

For

this reason there are no sinking fund or other fees.

The

funds go to the body corp to pay the insurance bill and the building insurance

is cheaper as a duplex than as two separate houses.

The building is a duplex only because the two buildings are joined by a fireproof

garage wall, maximizing the use of the land. These houses are houses in their

own right.

TWO

STRATA TITLED 4 BED HIGH SET STRATA TITLED UNITS WITH PROPERTY RETURNS OVER

$52,000 A YEAR.

AN

OPPORTUNITY HERE FOR AN ASTUTE INVESTOR – YIELDS OVER 5% EACH PROPERTY AND

INCOME

PRODUCING STRATA TITLED AIR-CONDITIONED 3 BEDROOM DUPLEX'S WITH STUDY NOOK

GREAT FOR YOUR SUPERANNUATION

PORTFOLIO! CAPITAL GROWTH ASSURED!

AND THE RENT HAS GOOD POTENTIAL TO MOVE UP 5-10%

IN THE HEART OF SPRINGWOOD

THESE DUPLEXES OFFER ALSO THE CHANCE FOR AN EXTENDED FAMILY TO LIVE TOGETHER OR

FOR AN ASTUTE INVESTOR TO CONTINUE TO RENT OUT BOTH PROPERTIES WHICH SET THE

PRECEDENT IN RENTS FOR THE SPRINGWOOD

LOCATION LOCATION LOCATION - SEIZE THIS FANTASTIC PROPERTY

INVESTMENT OPPORTUNITY....

EXECUTIVE STYLED INCOME PRODUCING STRATA TITLED

AIR-CONDITIONED 3 BEDROOM DUPLEX'S WITH STUDY NOOK PROPERTY INVESTMENT

OPPORTUNITY

We are marketing

these properties as Duplex's or a Units individually and the Vendor is happy to

discuss prices.

You have the

Opportunity to Buy One or Both Units.

AS INDIVIDUAL UNITS

OR PAIRS.

THE VENDOR WANTS

MID $500,000 A T/HOUSE FOR HIGH SET AND MID $400,000 EACH FOR LOW SET.

AS PAIRS - UP TO 5%

DISCOUNT

HIGH SET FROM

$1,120,000 DISCOUNT TO SAY $1,064,000

LOW SET FROM

$940,000 DISCOUNT TO SAY $893,000

We look forward to

hearing from you to open discussions and interest in these Valuable Investment

Opportunities, as individual Units or Pairs.

http://ljgrealestate.com.au/property/19-tower-street-springwood-qld-4127/

AT A GLANCE

• Property management & Sales of Tenanted Investment Properties is our

Speciality - Core Business.

• Individual solutions to fit our client's needs

• Body corporate management

• Competitive Commission Rates

• LET FEE FOR REFERRALS, We are a business built on 20 years of Referrals.

• NO Lease Renewal & Comparable Market Analysis’ Fees/Charges

• PHOTOS TAKEN ON ENTRY, tenants are shown about safety switches and water mains etc. We meet all tenants on site.

• Hands on approach to all Property Investment Management Matters.

Dedicated to implementing best practice, achieving set goals and encompassing a consistent approach to quality management and making effective use of all available technology. We recognize that tenants are customers too, treating them with any sort of disrespect would be detrimental to all property investor's. It is all about Attitude. We Aim to remove the hassle from Sales & Rentals.

• Individual solutions to fit our client's needs

• Body corporate management

• Competitive Commission Rates

• LET FEE FOR REFERRALS, We are a business built on 20 years of Referrals.

• NO Lease Renewal & Comparable Market Analysis’ Fees/Charges

• PHOTOS TAKEN ON ENTRY, tenants are shown about safety switches and water mains etc. We meet all tenants on site.

• Hands on approach to all Property Investment Management Matters.

Dedicated to implementing best practice, achieving set goals and encompassing a consistent approach to quality management and making effective use of all available technology. We recognize that tenants are customers too, treating them with any sort of disrespect would be detrimental to all property investor's. It is all about Attitude. We Aim to remove the hassle from Sales & Rentals.

Monday, July 8, 2019

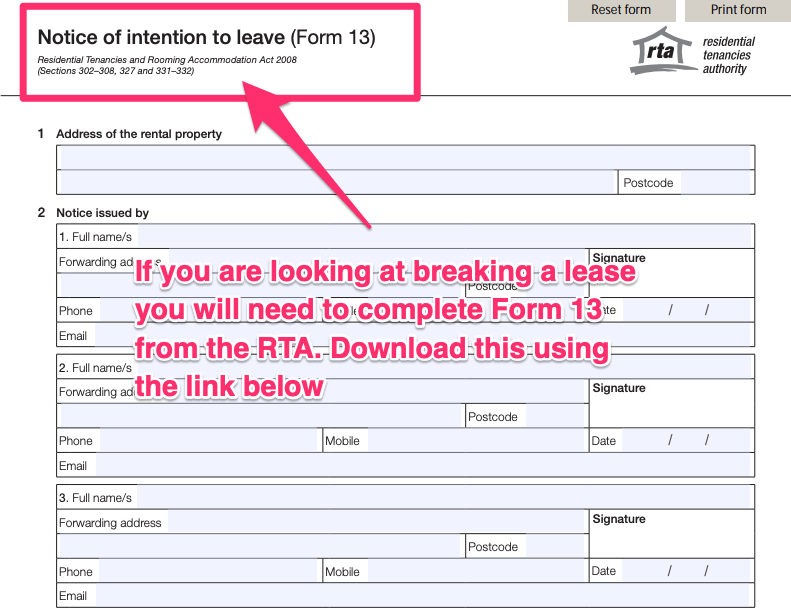

Can you break a lease when you buy a house?

Leases aren't meant to be broken but circumstances can always change.

http://ljgrealestate.com.au/competitive-commission/

http://ljgrealestate.com.au/property-management/

http://ljgrealestate.com.au/competitive-commission/

http://ljgrealestate.com.au/property-management/

When it comes to home ownership, timing can prove to be definitive.

Unfortunately, making a move on the perfect home can come at the expense of a leasing agreement.

If you're thinking about leaving behind your lease prematurely, it's best to know where you stand from a regulatory standpoint.

What does breaking the lease look like?

A lease is a legally binding agreement that comes with its own set of terms and conditions.

If a tenant decides to vacate a property before the end of the lease term (referred to as the fixed term agreement) without sufficient reason, they are breaking the lease or rental agreement.

The resulting loss of rent means compensation may need to be paid to the owner (or property manager).

According to the lease agreement, if a tenant leaves the rental property with two months left on the lease they technically owe the owner (or property manager) those two months rental even if they aren’t living there.

Breaking the news about breaking the lease

Both tenants and landlords must notify the other party in writing if they intend to terminate the lease.

As a tenant, if you want to notify the landlord of your intention to leave, complete a Form 13.

Supplied: Hunter Galloway

In Queensland, this is done through the Residential Tenancies Authority of Queensland (RTA), with a tenant providing Notice of Intention to leave to a property manager/owner when they want to vacate the property by a certain date.

A completed Form 13 is required to end a periodic agreement (i.e. if you’re paying month to month), end a fixed term agreement (i.e. if you have X months left on your lease), or ff they have grounds to end a fixed term agreement early, or if they are breaking the lease.

Tenants must send the form to the property manager for processing.

Reasons why a lease might be terminated

Some circumstances are unavoidable. The death of a sole tenant or a mortgagee giving notice are among the reasons why a lease might be terminated.

For first home buyers, the most realistic option is a written agreement between them and the landlord that the leasec is over.

Do I need to pay any costs when breaking my lease?

According to the RTA, the tenant may be asked to pay:

- Reasonable re-letting costs – usually one week’s rent plus GST

- Reasonable advertising costs (if incurred), and

- Compensation for loss of rent – until a new tenant is found or until the end date of the agreement whichever happens first.

The property manager or owner is legally required to minimise the costs associated with breaking the lease. At any time if the tenant feels that the property manager or owner are not mitigating this loss, contact the RTA for help.

What could these costs potentially look like?

Let’s run with the above scenario, the tenant has found the perfect home but has two months left on their lease which costs $500 per week.

Worst case scenario is that they might be required to cover:

- Reasonable re-letting costs – one week's rent = $500

- Reasonable advertising costs = $100

- Compensation for loss of rent = It took four weeks to find a new tenant 4 x $500 = $2,000

So it could cost the tenant an extra $2,600 in rent to break their lease early to buy a home.

What are some ways you can break the lease without costs?

There are ways to soften the financial blow that comes with breaking the lease agreement.

Giving the landlord adequate notice and helping them find a replacement tenant are examples of this.

Other ways to minimise the costs associated with breaking a lease include:

- Reducing advertising costs – Can also be reduced as the tenant should only be reasonably expected to contribute to the advertising costs. What this means is if the tenant has 50 per cent of their lease left, say they are six months into a 12-month lease, the tenant should only pay 50 per cent of the advertising fee. If they have three months left on a 12-month lease then they should only pay 25 per cent, etc.

- Check for a break of contract – As part of the lease, the property owner agrees to maintain the property and provide a safe environment. Unfortunately not every property owner lives up to their side of the deal, and if they ignore requests to fix broken appliances, sort dodgy plumbing or if there is mould or insect problems, the tenant could say they have breached their lease contract.

If the property manager and tenant mutually agree, any tenancy agreement can be terminated at any time. So these figures are the worst case, but its worth having a chat with the property manager to see what can be worked out.

When is my tenancy agreement terminated?

Legally speaking, the lease is not broken until the tenant has given back vacant possession of the rental property – i.e. they've completely moved out.

If the tenant believes they've been placed under excessive hardship by the property manager or owner, they can apply for excessive hardship through QCAT provided they have evidence to support the application.

AT A GLANCE

• Property management & Sales of Tenanted Investment Properties is our Speciality - Core Business.

• Individual solutions to fit our client's needs

• Body corporate management

• Competitive Commission Rates

• LET FEE FOR REFERRALS, We are a business built on 20 years of Referrals.

• NO Lease Renewal & Comparable Market Analysis’ Fees/Charges

• PHOTOS TAKEN ON ENTRY, tenants are shown about safety switches and water mains etc. We meet all tenants on site.

• A hands-on approach to all Property Investment Management Matters.

Dedicated to implementing best practice, achieving set goals and encompassing a consistent approach to quality management and making effective use of all available technology. We recognize that tenants are customers too, treating them with any sort of disrespect would be detrimental to all property investors. It is all about Attitude. We Aim to remove the hassle from Sales & Rentals.

• Property management & Sales of Tenanted Investment Properties is our Speciality - Core Business.

• Individual solutions to fit our client's needs

• Body corporate management

• Competitive Commission Rates

• LET FEE FOR REFERRALS, We are a business built on 20 years of Referrals.

• NO Lease Renewal & Comparable Market Analysis’ Fees/Charges

• PHOTOS TAKEN ON ENTRY, tenants are shown about safety switches and water mains etc. We meet all tenants on site.

• A hands-on approach to all Property Investment Management Matters.

Dedicated to implementing best practice, achieving set goals and encompassing a consistent approach to quality management and making effective use of all available technology. We recognize that tenants are customers too, treating them with any sort of disrespect would be detrimental to all property investors. It is all about Attitude. We Aim to remove the hassle from Sales & Rentals.

Best Regards

Linda 姬琳达珍 and Carlos Debello (LREA)

LJ Gilland Real Estate Pty Ltd

PO BOX 19

ZILLMERE 4034

Ph: 07 3263 6085

ZILLMERE 4034

Ph: 07 3263 6085

0413 560 808

0400 833 800

0409 995 578 (L)

Wednesday, July 3, 2019

Tuesday, July 2, 2019

Rental report shows growth in Perth and Brisbane The CoreLogic Quarterly Rental Review shows national weekly rents increased by 0.3 per cent over the second quarter of 2019, led by increases in the Brisbane and Perth markets.

Rental report shows growth in Perth and Brisbane

The CoreLogic Quarterly Rental Review shows national weekly rents increased by 0.3 per cent over the second quarter of 2019, led by increases in the Brisbane and Perth markets.

Sydney and Darwin were the only capital cities where rents declined across the June quarter, according to a new report.

CoreLogic's Quarterly Rental Review indicates capital city rents were 0.1 per cent higher over the quarter and -0.1 per cent lower year-on-year while the regional market rents were 0.7 per cent higher over the quarter to be 1.9 per cent higher over the past 12 months.

Brisbane and Perth were the only two capitals where the annual change in rents over the past year was superior to growth over the same period in 2018.

CoreLogic research analyst Cameron Kusher said the rental market remained quite mixed overall.

"It is clear that Sydney accounts for a large share of overall renters with annual falls in Sydney leading to a fall in the combined capital city index," he said.

“Sydney and Melbourne continue to experience the impact of heightened demand from investors over recent years along with a substantial ramp-up in new housing (largely apartment) supply, much of which was purchased by investors. “The past year has seen a change of direction for both the Brisbane and Perth rental markets, which are now climbing again following years of decline."

At the end of the 2018-19 financial year, national rents were recorded at $438/week.

Rental rates across the combined capital cities sat at $466/week and substantially higher than the $380/week across the combined regional markets.

Sydney remains the most expensive city to rent a property at $580/per week.

Mr Kusher said there had been a changing of the guard when it came to the most affordable city to rent.

"For many years Hobart has been the most affordable rental market," he said.

"However, the rapid growth in rents over recent years has seen it become more expensive than Brisbane, Adelaide, Perth and Darwin and on par with the cost of renting in Melbourne.”

Housing affordability marginally improved across the country in the March quarter 2019 with the exception of the Northern Territory, according to research from the Real Estate Institute of Australia and Adelaide Bank.

REIA President Adrian Kelly said the March quarter 2019 edition of the Adelaide Bank/REIA Housing Affordability Report found New South Wales had the largest improvement in housing affordability with a 1.3 per cent decrease in home loan repayments.

“While rental affordability improved marginally in the larger states of New South Wales, Victoria and Queensland as well as in Western Australia and the Northern Territory, a large decline in rental affordability in South Australia and Tasmania offset this improvement resulting in an overall decline in rental affordability nationally,” he said.

According to the report the total number of loans declined (excluding refinancing) decreased to 86,909, a decline of 20.0 per cent over the March quarter.

“This is not unusual for the first quarter of the calendar year, however, compared with the same quarter of 2018, the number of new loans declined by 13.7 per cent,” Mr Kelly said.

“The number of those entering the home loan market also declined over the year. Interestingly, while loan size decreased for changeover buyers, it increased marginally for first home buyers.”

Mr Kelly noted that the RBA’s decision yesterday to cut interest rates by 25 basis point rates will see a further improvement in affordability.

“Subject to the banks passing on the full cut, for a first home buyer this means a saving of $70 per month based on an average loan size of $338k in the March quarter of 2019," he said.

New South Wales

Over the March quarter, housing affordability in New South Wales improved with the proportion of income required to meet loan repayments decreasing to 35.4 per cent, a decrease of 1.3 percentage points over the quarter. Housing affordability also improved over the past year with proportion of income required to meet monthly loan repayments decreasing by 1.1 percentage points.

In New South Wales, the number of loans to first home buyers decreased to 5,790, a decrease of 24.2 per cent over the quarter and a decrease of 11.0 per cent compared to the March quarter 2018.

Rental affordability improved marginally in New South Wales over the March quarter with the proportion of income required to meet median rent payments decreasing to 28.2 per cent, a decrease of 0.1 percentage points over the March quarter and 1.9 percentage points compared with the March quarter 2018.

Victoria

Over the March quarter, housing affordability improved in Victoria with the proportion of income required to meet loan repayments decreasing to 32.5 per cent, a decrease of 0.6 percentage points over the quarter and 1.6 percentage points compared to the same quarter of the previous year.

The number of loans to first home buyers in Victoria decreased to 7,199, a decrease of 18.7 per cent over the quarter, and a decrease of 11.9% compared to the March quarter 2018. In Victoria, the total number of loans (excluding refinancing) decreased to 24,566, a decrease of 20.4 per cent during the quarter.

Rental affordability in Victoria improved over the March quarter with the proportion of income required to meet median rent decreasing marginally to 23.1 per cent, a decrease of 0.1 percentage points over the quarter and 0.7 percentage points compared with the March quarter 2018.

Queensland

Housing affordability in Queensland improved with the proportion of income required to meet loan repayments decreasing to 27.5%, a decrease of 0.6% over the quarter but remaining steady compared to the same quarter last year.

Over the March quarter, the number of loans to first home buyers in Queensland decreased to 4,677, a decrease of 17.4 per cent over the quarter and a decrease of 17.1 per cent compared to the same quarter of 2018. The number of loans (excluding refinancing) decreased in Queensland to 17,979, a decrease of 16.9 per cent over the quarter and a decrease of 14.9 per cent compared to the March quarter of the previous year.

Rental affordability in Queensland also improved over the quarter with the proportion of income required to meet the median rent decreasing to 22.0 per cent, a decrease of 0.1 percentage points over the quarter and a decrease of 1.1 percentage points over the past year.

South Australia

Over the March quarter, housing affordability in South Australia improved with the proportion of income required to meet monthly loan repayments decreasing to 26.9 per cent, a decrease of 0.6 percentage points over the quarter and 0.3 percentage points compared to the March quarter in 2018.

Over the March quarter, the number of loans to first home buyers in South Australia decreased to 1,370, a decrease of 16.7 per cent over the quarter but an increase of 5.6 per cent compared to the March quarter 2018. In South Australia, the total number of loans (excluding refinancing) decreased to 6,503, a decrease of 14.5% over the quarter, and a decrease of 2.0 per cent compared to the March quarter 2018.

Rental affordability in South Australia declined over the quarter with the proportion of income required to meet average rent payments increasing to 22.8 per cent, an increase of 0.8 percentage points over the quarter and an increase of 0.4 percentage points compared to the same quarter in 2018.

Western Australia

Over the March quarter, housing affordability in Western Australia improved with the proportion of income required to meet loan repayments decreasing to 22.6 per cent, a decrease of 0.5 percentage points over the quarter and a decrease of 1.0 percentage points over the previous year.

The number of first home buyers in Western Australia decreased to 3,313 in the March quarter, a decrease of 13.6 per cent over the quarter and a decrease of 7.4 per cent compared to the same time last year. The total number of loans (excluding refinancing) in Western Australia decreased to 9,235, a decrease of 16.2 per cent over the quarter and a decrease of 9.3 per cent compared to the same time last year.

Rental affordability in Western Australia also improved during the March quarter with the proportion of income required to meet the median rent decreasing to 16.5 per cent, a decrease of 0.1 percentage points over the quarter. However, rental affordability declined over the past year with the proportion of income required to meet median rent increasing 0.2 percentage points.

Tasmania

Over the March quarter, housing affordability in Tasmania improved with the proportion of income required to meet loan repayments decreasing to 25.4 per cent, a decrease of 0.9 percentage points over the quarter. However, housing affordability has declined over the past year with the proportion of income required to meet monthly loan repayments increasing by 0.9 percentage points.

The number of first home buyers in Tasmania decreased to 475, a decrease of 12.8 per cent over the quarter but an increase of 13.1 per cent compared to the same quarter of the previous year. The total number of new loans (excluding refinancing) in Tasmania decreased to 2,245, a decrease of 12.9 per cent

over the quarter but an increase of 4.5 per cent compared to the corresponding quarter 2018.

over the quarter but an increase of 4.5 per cent compared to the corresponding quarter 2018.

Rental affordability in Tasmania declined over the quarter with the proportion of income required to meet median rents increasing to 29.3 per cent, an increase of 1.2 percentage points over both the quarter and when compared to the same period in 2018.

Northern Territory

Over the March quarter, housing affordability in the Northern Territory declined with the proportion of income required to meet loan repayments increasing to 20.2 per cent, an increase of 0.8 percentage points over the quarter and an increase of 0.4 percentage points when compared to the March quarter 2018.

The number of loans to first home buyers in the Northern Territory decreased to 187, a decrease of 28.4% over the March quarter but an increase of 12.7% compared to the March quarter 2018. The number of new loans (excluding refinancing) in the Northern Territory decreased to 506, a decrease of 22.0 per cent over the quarter and a decrease of 17.6 per cent compared to the March quarter 2018.

Rental affordability in the Northern Territory improved during the March quarter with the proportion of income required to meet the median rent decreasing to 20.9 per cent, a decrease of 0.4 percentage points over the quarter and 1.6 percentage points over the previous year.

Australian Capital Territory

Over the March quarter, housing affordability in the Australian Capital Territory improved with the proportion of income required to meet loan repayments decreasing to 20.3 per cent, a decrease of 0.3 percentage points over the quarter.

The number of loans to first home buyers in the Australian Capital Territory decreased to 392, a decrease of 44.8 per cent over the quarter, and a decrease of 43.0 per cent compared to the March quarter 2018. The number of loans (excluding refinancing) in the Australian Capital Territory decreased to 1,952, a decrease of 31.0 per cent over the quarter and a decrease of 14.9 per cent compared to the March quarter 2018.

Rental affordability in the Australian Capital Territory has declined over the quarter with the proportion of income required to meet the median rent increasing to 19.0%, an increase of 0.1 percentage points over the quarter and an increase of 0.5 percentage points over the past year.

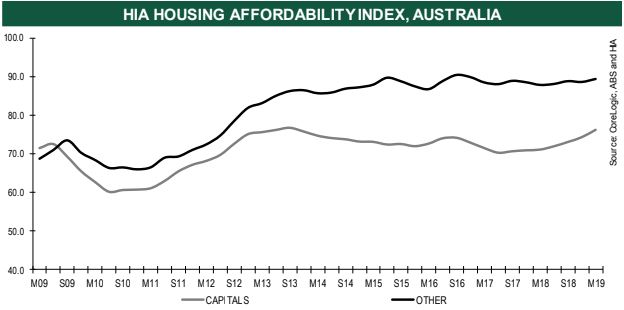

The sharpest rise in housing affordability since 2013 is a result of the "pent up" demand experienced in Sydney and Melbourne throughout the past two decades finally being met, according to the Housing Industry Association.

The HIA Affordability Index rose by 2.2 per cent in the March 2019 quarter to post the most significant improvement in affordability for nearly six years.

The index is calculated for each of the eight capital cities and regional areas on a quarterly basis and takes into account the latest dwelling prices, mortgage interest rates and wage developments.

At a glance:

- The HIA Affordability Index rose by 2.2 per cent in the March 2019 quarter, representing the sharpest increase since September, 2013.

- According to HIA, the improvement was most significant in the east coast cities.

- The boom in home building across the past five years is believed to have been a factor in the trend.

HIA Chief Economist Tim Reardon told WILLIAMS MEDIA the rise had come from the supply of new homes finally catching up with demand.

"We had 20 years of mismanagement when it came to the supply of new homes, which meant there weren't enough homes to satisfy demand, and house prices went up as a result," he said.

"Now we are seeing a sufficient number of homes being built to meet demand, meaning that new home building has declined significantly."

In its quarterly economic and industry outlook released last week, HIA's preliminary data suggested that the housing market has adjusted from a strong annualised rate of home building of around 220,000 homes per year this time last year, to around 183,000 at the start of 2019.

Mr Reardon said while the correction had occurred much quicker than they had anticipated, the historical context of the data had to be taken into account.

"What we've found is that consumers are very poor at picking the bottom of the housing price cycle," he said.

"We usually only know what the bottom was three to six months after we have been there.

"For home builders, the correction occurring in the market is quite painful, but from a national policy perspective, this is the sharpest downturn we have seen in 20 years to what will be the shallowest drop.

"It's been a sharp rate of decline, but we will probably end up where we were in 2012/13 which, at the time, were fairly reasonable years.

Source: HIA

Rapid east coast improvement

According to the HIA Affordability Index, improvement in housing affordability has been experienced across the country, with the exception only of Tasmania and the ACT, where ongoing house price growth has seen affordability remain static.

Mr Reardon was most significant in the east coast capital cities.

"Affordability in Sydney deteriorated to an extent that in June 2017 it required two average Sydney incomes to be able to afford repayments on an average Sydney home," he said.

"In just over a year this has improved to only requiring 1.8 standard incomes to purchase the same home.

“Similarly, in Melbourne, the Affordability Index has improved by almost 10 per cent in a year."

Five of the eight capital cities saw improved affordability over the year to March 2019. Sydney continues to be home to the greatest improvements, its index is up by 12.4 per cent.

This was followed by Melbourne (+9.6 per cent), Perth (+7.7 per cent), Darwin (+5.9 per cent) and Brisbane (+2.5 per cent). Affordability deteriorated in Hobart (-5.1 per cent), Canberra (-5.1 per cent) and Adelaide (-1.1 per cent).

Best Regards

Linda 姬琳达珍 and Carlos Debello (LREA)

LJ Gilland Real Estate Pty Ltd

Subscribe to:

Posts (Atom)